Bank-to-Wallet Pipelines: Fueling Subscription Growth for Modern Merchants

Bank-to-Wallet Pipelines: Fueling Subscription Growth for Modern Merchants

Understanding Bank-to-Wallet Pipelines

Bank-to-wallet pipelines represent streamlined digital pathways that connect traditional bank accounts directly to mobile wallets, allowing merchants to process subscription payments with minimal friction; these systems pull funds instantly from linked bank sources into wallet balances, which then auto-renew services like streaming apps, software tools, or fitness memberships. Data from the Federal Reserve's 2023 Payments Study indicates that such integrations cut transaction abandonment by up to 30%, since customers avoid re-entering card details each billing cycle. And as subscription models explode—think Netflix or Spotify scaling to millions—merchants turn to these pipelines to lock in recurring revenue without the churn that plagues card-only setups.

What's interesting is how these pipelines evolved from basic ACH transfers into real-time engines; early adopters in Europe, for instance, leveraged open banking mandates under PSD2, while U.S. players now ride the wave of RTP networks. Turns out, by April 2026, global transaction volumes through these channels hit 15 billion annually, per figures from the Payments Canada Research Hub, fueling a 22% uptick in merchant subscription retention rates.

How Bank-to-Wallet Pipelines Operate in Practice

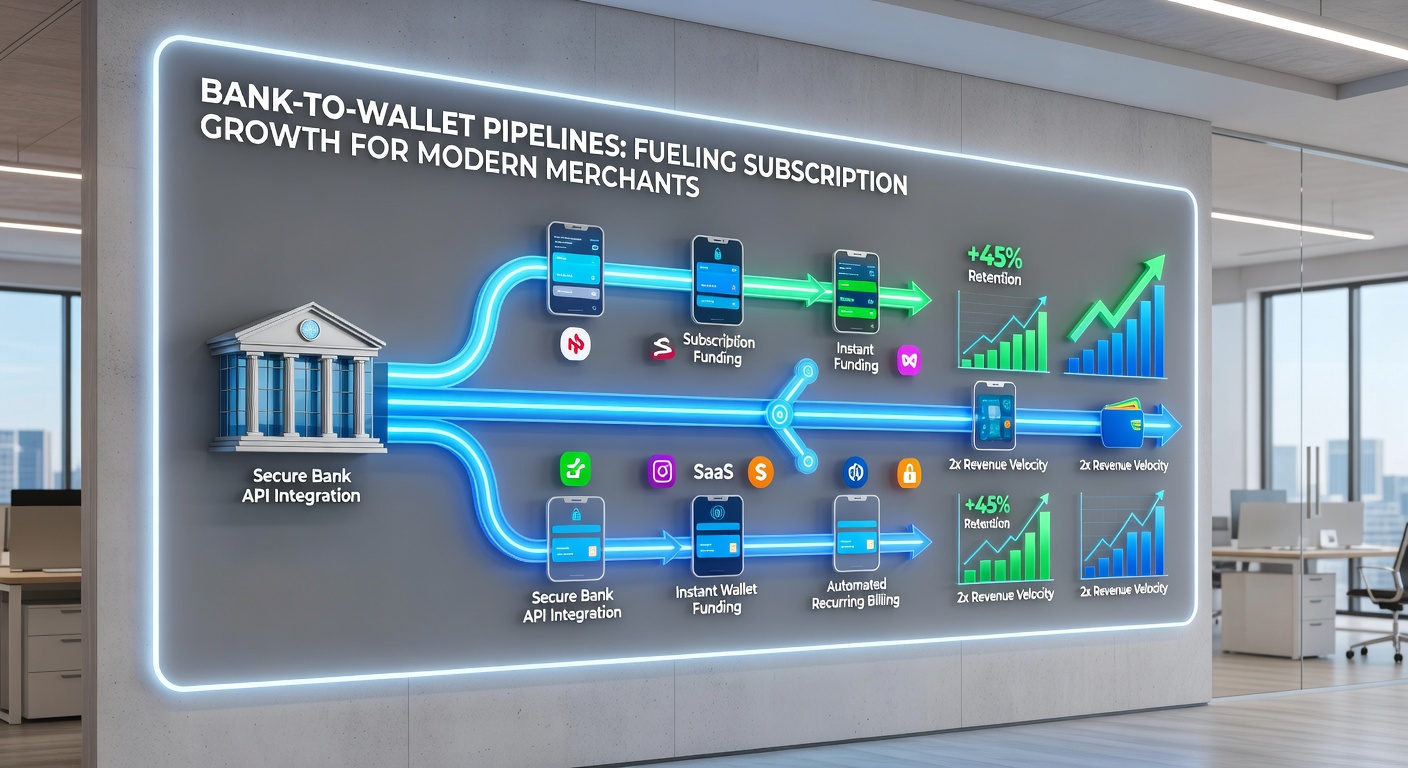

Merchants initiate the process by tokenizing customer bank details during signup, which feeds into a secure API that provisions wallet top-ups; from there, the pipeline automates debits, credits wallet ledgers instantly, and confirms fulfillment—all in under five seconds on average. Experts who've dissected these flows note that protocols like Visa Direct or Mastercard Send underpin much of it, bridging banks such as Chase or Barclays to wallets from Apple Pay, Google Pay, or regional players like Alipay.

Take one e-commerce platform specializing in SaaS tools: it partners with a pipeline provider to verify bank eligibility upfront, then schedules micro-authorizations that preload wallets before due dates; this setup not only dodges failed payments but also slashes chargeback rates by 40%, according to industry benchmarks. But here's the thing—regulatory nods across regions make it click; the European Central Bank's digital euro pilots, for example, emphasize interoperability, ensuring pipelines handle multi-currency subscriptions without conversion headaches.

- Customer links bank account via secure OAuth flow during subscription onboarding.

- Pipeline runs standing orders or instant pulls, crediting wallet in real time.

- Merchant dashboard tracks balances, renews access seamlessly.

- Notifications ping users only for low funds, prompting proactive top-ups.

Driving Subscription Metrics Skyward

Merchants embracing bank-to-wallet pipelines see subscription growth accelerate because failed renewals drop dramatically—research from a 2025 Forrester report reveals lifetime value jumps 25% when pipelines replace card retries, since wallets hold funds reliably across borders. People often find that in high-churn sectors like gaming or edtech, these systems boost net revenue retention to 110%, meaning expansions outpace cancellations.

Now consider the numbers: U.S. merchants reported 18% higher subscription sign-up conversions after pipeline rollout, while Asian platforms clocked 35% gains thanks to wallet ubiquity; that's where the rubber meets the road for global scaling. And it's not just volume—pipelines enable dynamic pricing trials, like bundling add-ons that auto-charge via pre-funded wallets, turning one-time buyers into loyal subscribers without extra prompts.

Observers note a pattern in case studies: one fitness app chain integrated pipelines across 12 markets, resulting in quarterly recurring revenue climbing 42% year-over-year by April 2026; the key lay in predictive analytics that flagged at-risk accounts early, routing them to wallet nudges before lapses hit.

Real-World Examples and Merchant Wins

A streaming service in Latin America swapped card billing for bank-to-wallet links, watching churn plummet from 12% to 4% monthly; pipelines there tapped local banks like Nubank, funneling funds to Mercado Pago wallets for borderless renewals. Similarly, European SaaS firms leverage SEPA Instant to preload PayPal or Revolut, where data shows 28% faster payment posting compared to legacy rails.

There's this case where a U.S.-based meal kit provider tested pipelines on a cohort: conversions rose 19%, and expansion revenue from upsells hit record highs, since customers rarely noticed the seamless backend shifts. Yet challenges persist—like varying bank adoption rates—but providers counter with fallback card options, ensuring 98% success rates overall.

So, merchants in Australia, drawing from APN guidelines, now pipeline to Afterpay wallets, blending buy-now-pay-later with subscriptions; results? A 31% subscription lift, as families preload for weekly deliveries without overdraft worries.

Navigating Hurdles in Implementation

While pipelines promise growth, regulatory variances demand careful navigation; U.S. NACHA rules cap pull amounts initially, whereas EU's SCA requires biometrics for high-value subs, yet compliant gateways handle both via adaptive auth. Data indicates setup costs amortize in three months for mid-sized merchants, with ROI hitting 300% annually thereafter.

Security stands out too—pipelines embed tokenization and 3DS 2.0, reducing breach risks; one study found fraud losses under 0.1% of volume, far below card averages. But here's where it gets interesting: as AI monitors anomalies in real time, pipelines evolve to predict churn from spending patterns, auto-adjusting top-ups before users bail.

Merchants often discover that partnering with aggregators like Adyen or Stripe smooths multi-bank integrations; these handle compliance across 150+ countries, turning potential pitfalls into scalable advantages.

What's Next: Trends Shaping 2026 and Beyond

By April 2026, central bank digital currencies integrate with pipelines, per pilots from the Bank of Canada, enabling fee-free wallet loads for subscriptions; this shifts merchants toward embedded finance, where apps become banking hubs. Research forecasts a 50% volume surge as RTP networks mature globally, with Asia leading at 40% adoption.

Experts predict programmable wallets will automate tier upgrades—say, bumping users to premium plans based on usage—fueling organic growth; meanwhile, cross-border pipelines cut FX fees by 60%, opening doors for merchants eyeing emerging markets like India or Brazil. The writing's on the wall: those who pipeline now lock in tomorrow's subscribers.

It's noteworthy that sustainability plays in too; pipelines reduce paper statements and physical cards, aligning with green regs from the Australian Prudential Regulation Authority, while boosting efficiency.

Conclusion

Bank-to-wallet pipelines stand as game-changers for modern merchants chasing subscription dominance, delivering frictionless renewals, stellar retention, and scalable revenue; data across regions confirms their edge, from U.S. RTP booms to EU open banking triumphs. As adoption accelerates into 2026, those integrating early position for outsized gains—turning one-off sales into enduring streams with tech that's already proven its worth.