Case Studies Revealing How Merchant Accounts Coordinate Credit Authorizations with Digital Wallet Payouts During High-Volume Subscription Cycles Across Multiple Currencies

Merchant accounts handle credit authorizations by first validating card details through acquiring banks then confirming available funds before any subscription cycle begins and this process links directly to digital wallet payouts when recurring charges trigger automatic transfers in multiple currencies.

Coordination Mechanisms in Subscription Processing

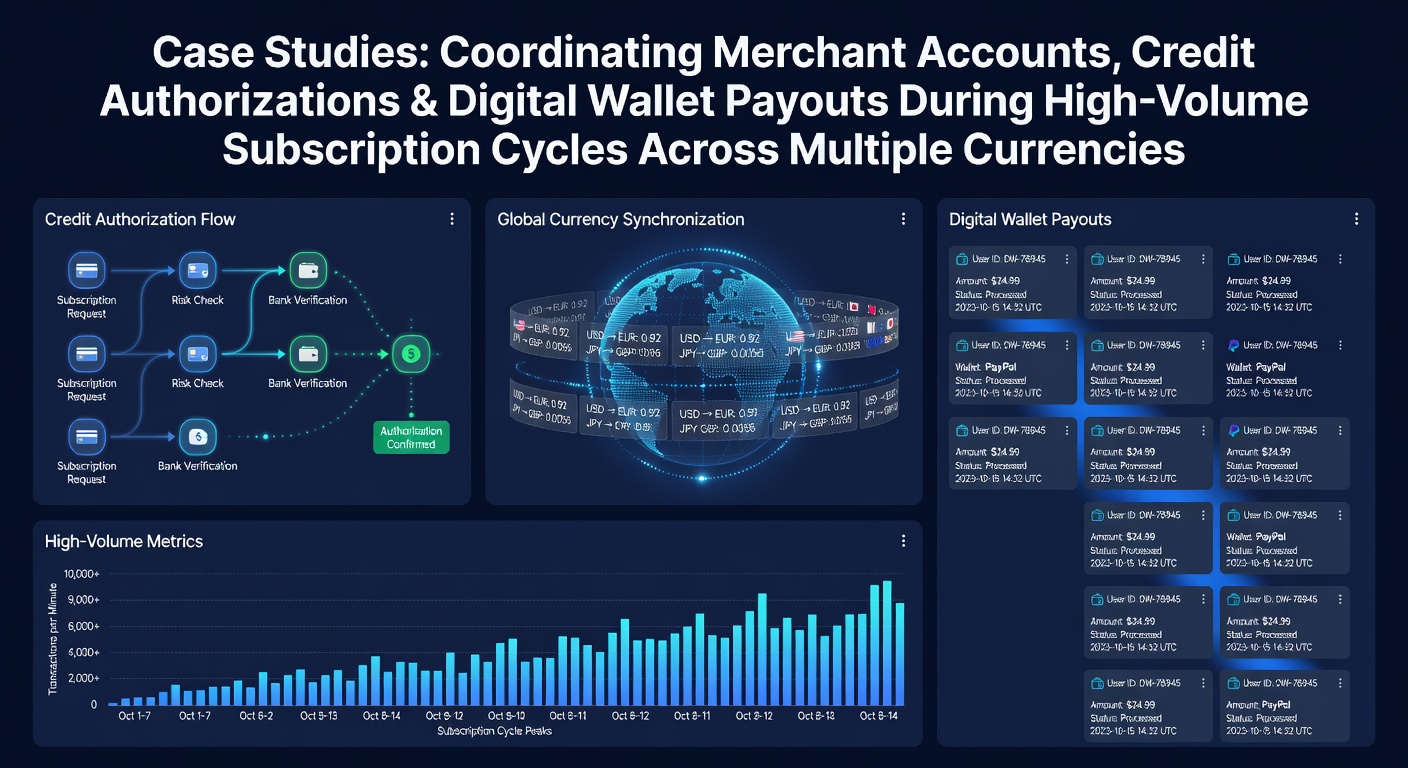

Systems synchronize authorization requests with payout instructions by routing credit card approvals through payment processors that then trigger wallet disbursements once settlement occurs and observers note that timing becomes critical during peak subscription renewals when thousands of transactions process simultaneously across regions. Data from mid-2026 indicates that platforms managing high-volume cycles often batch authorizations in hourly windows which allows wallets to receive funds in the originating currency before conversion applies to the merchant's primary ledger.

One documented case involved a European streaming service handling subscriptions in euros, British pounds, and Japanese yen where the merchant account coordinated pre-authorizations on credit cards 48 hours before due dates and wallet payouts executed immediately after successful captures to maintain liquidity for content licensing fees.

Multi-Currency Handling During Peak Cycles

High-volume periods such as annual renewals in June 2026 tested coordination protocols when exchange rate fluctuations required real-time adjustments between authorization amounts and final wallet credits and researchers documented how merchant accounts used dynamic currency conversion tools to lock rates at authorization time rather than settlement. This approach reduced discrepancies that otherwise arise when wallets operate in local denominations while credits flow through international acquiring networks.

Another case study focused on a North American software provider managing subscriptions across US dollars, Canadian dollars, and Australian dollars and the account employed reconciliation APIs that matched each credit authorization token with corresponding wallet payout references which prevented double-booking during spikes exceeding 50,000 transactions per day.

According to findings published by the Bank for International Settlements, coordination layers between merchant accounts and wallet providers rely on standardized messaging formats that embed currency identifiers early in the authorization sequence and this enables seamless handoffs when payouts cross borders.

Case Examples from Different Sectors

A subscription box company operating in Asia-Pacific regions demonstrated coordination by pre-authorizing credit cards in local currencies then directing payouts to digital wallets held by suppliers in Singapore dollars and Malaysian ringgit and the process used automated rules that adjusted for settlement delays common in cross-border acquiring. The merchant account maintained separate ledgers for each currency pair which allowed quick identification of any mismatches during high renewal volumes.

Yet another example came from a Canadian educational platform that processed recurring payments in multiple currencies through merchant accounts integrated with wallet services and data showed successful synchronization when authorization holds converted to actual captures aligned precisely with payout triggers to supplier accounts. Research from the Reserve Bank of Australia highlights similar patterns where timing protocols reduced failed payout rates by aligning credit network confirmations with wallet system acknowledgments.

Reconciliation and Settlement Practices

Daily reconciliation routines compare authorization logs against wallet payout records and merchant accounts flag variances for manual review while automated systems handle the bulk of matches during subscription cycles and this practice proves essential when volumes surge and currency conversions introduce rounding differences. Case studies reveal that platforms often run parallel verification checks one through the credit network adn another via the wallet provider to ensure end-to-end accuracy.

Those managing these flows report that integration points between authorization gateways and payout engines require precise timestamp synchronization because even minor offsets can disrupt reporting for high-volume merchants operating across time zones.

Conclusion

Case studies illustrate that merchant accounts achieve effective coordination between credit authorizations and digital wallet payouts through synchronized timing, currency-specific ledgers, and automated reconciliation tools especially during intense subscription cycles spanning multiple currencies. Evidence from 2026 operations shows these methods support consistent processing even as transaction volumes grow and regulatory frameworks evolve across regions.