How Verification Protocols Enhance Reliability in Electronic Fund Movement Systems for Commercial Entities

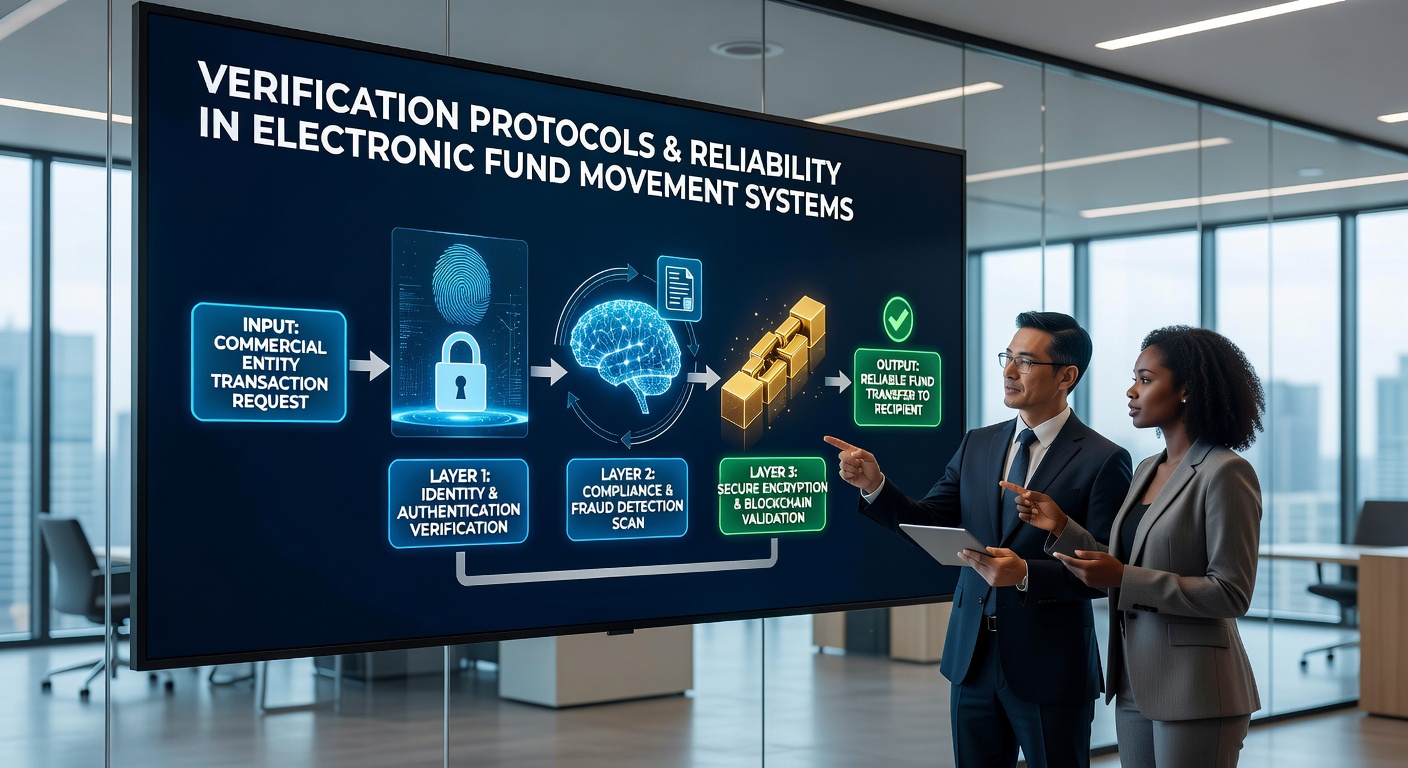

Electronic fund movement systems handle billions in daily transactions for businesses around the world, yet their reliability depends heavily on layers of verification that confirm identities, validate amounts, and cross-check destinations before any value shifts between accounts. Commercial entities rely on these protocols to keep payment streams consistent across supply chains, vendor settlements, and payroll distributions where even small discrepancies can cascade into operational delays. Researchers at institutions tracking payment infrastructure note that protocols such as digital signatures, tokenization, and real-time account validation work together to create checkpoints that reduce both accidental errors and deliberate interference. These mechanisms operate at multiple stages of a transfer. Initial authentication verifies the sending party's credentials through multi-factor methods that combine passwords with device-based tokens or biometric checks, while subsequent authorization layers confirm that the requested amount aligns with pre-approved limits set by the organization. Data from the Federal Reserve indicates that systems incorporating these steps experience fewer failed transactions because mismatched details trigger immediate alerts rather than post-settlement corrections.

Electronic fund movement systems handle billions in daily transactions for businesses around the world, yet their reliability depends heavily on layers of verification that confirm identities, validate amounts, and cross-check destinations before any value shifts between accounts. Commercial entities rely on these protocols to keep payment streams consistent across supply chains, vendor settlements, and payroll distributions where even small discrepancies can cascade into operational delays. Researchers at institutions tracking payment infrastructure note that protocols such as digital signatures, tokenization, and real-time account validation work together to create checkpoints that reduce both accidental errors and deliberate interference. These mechanisms operate at multiple stages of a transfer. Initial authentication verifies the sending party's credentials through multi-factor methods that combine passwords with device-based tokens or biometric checks, while subsequent authorization layers confirm that the requested amount aligns with pre-approved limits set by the organization. Data from the Federal Reserve indicates that systems incorporating these steps experience fewer failed transactions because mismatched details trigger immediate alerts rather than post-settlement corrections.Key Verification Layers in Commercial Transfers

Tokenization replaces sensitive account numbers with unique identifiers that hold no standalone value, allowing commercial platforms to process recurring payments without exposing full banking details during each cycle. When combined with checksum algorithms that validate routing numbers and account sequences, this approach catches formatting mistakes before funds leave the originating institution. Observers at the European Central Bank have documented how such layered checks contribute to higher straight-through processing rates in cross-border corporate payments, where currency conversions and intermediary banks add complexity.

Real-time verification extends further by querying receiving accounts for confirmation of ownership and status, a practice that gained wider adoption after infrastructure updates rolled out in early 2026. Companies handling high-volume vendor payments now integrate these queries directly into their enterprise resource planning tools, which means a transfer request pauses automatically if the destination account shows recent closures or restrictions. This step prevents funds from entering limbo accounts that require manual recovery later.

Effects on Operational Consistency

Commercial entities that embed verification protocols throughout their electronic movement workflows report steadier cash flow timing because fewer transactions require reversal or re-initiation. Protocols that reconcile batch totals against individual line items before release also help accounting teams match outgoing payments with invoices in near real time. Studies from payment research groups show that organizations using synchronized verification across internal ledgers and external networks cut reconciliation time by noticeable margins, freeing staff for higher-value analysis instead of error chasing.

Encryption standards wrapped around every message ensure that details remain unaltered during transit, while digital certificates issued by trusted authorities confirm the identity of both sending and receiving systems. In practice this means a procurement department authorizing a large equipment purchase can track the payment's journey through each intermediary without uncertainty about whether the amount or beneficiary changed en route. The result appears in audit trails that regulators and internal compliance officers can review quickly when questions arise.

Integration with Existing Business Systems

Many commercial platforms now connect verification services directly to their treasury management software, creating automated sequences that run every time a payment file is generated. These sequences flag unusual patterns, such as sudden changes in payment frequency or destination country, and route them for additional human review before processing continues. Data compiled by industry associations tracking corporate treasury practices highlights that such integrations reduce exception handling volumes, particularly for firms operating across multiple jurisdictions where regulatory requirements differ.

API-based verification calls allow smaller merchants and mid-sized suppliers to access the same protective layers once reserved for large banks, leveling participation in electronic movement networks. When a supplier uploads an invoice through a connected portal, the system immediately validates bank details against official registries maintained by central banks or clearing houses, which minimizes returns caused by outdated information. This connectivity proves especially useful during periods of account migrations or mergers that frequently alter beneficiary details.

Regulatory Alignment and Reporting Benefits

Verification protocols also support compliance reporting because each checked transfer generates immutable logs that satisfy record-keeping mandates from authorities in different regions. The Bank of Canada, for example, encourages participants in its large-value transfer system to maintain verifiable audit paths that demonstrate authorization at every step. Similar expectations appear in guidelines issued by the Reserve Bank of Australia, where entities must show evidence that recipient details were confirmed before settlement occurs.

These requirements encourage broader adoption of standardized verification methods across borders, which in turn improves interoperability between domestic and international networks. Commercial entities gain from the consistency because they can apply one set of internal controls rather than maintaining separate procedures for each market they serve.

Conclusion

Verification protocols continue to strengthen the foundation of electronic fund movement systems used by commercial entities through consistent application of authentication, validation, and reconciliation steps. As infrastructure evolves through 2026 and beyond, these measures support smoother operations by catching discrepancies early and maintaining clear records that meet both business and regulatory needs. Organizations that maintain robust verification practices position their payment flows for sustained reliability across changing market conditions.