The Mechanics of Authorization Layers in Portable Payment Applications Supporting Subscription Models for Businesses Operating Internationally

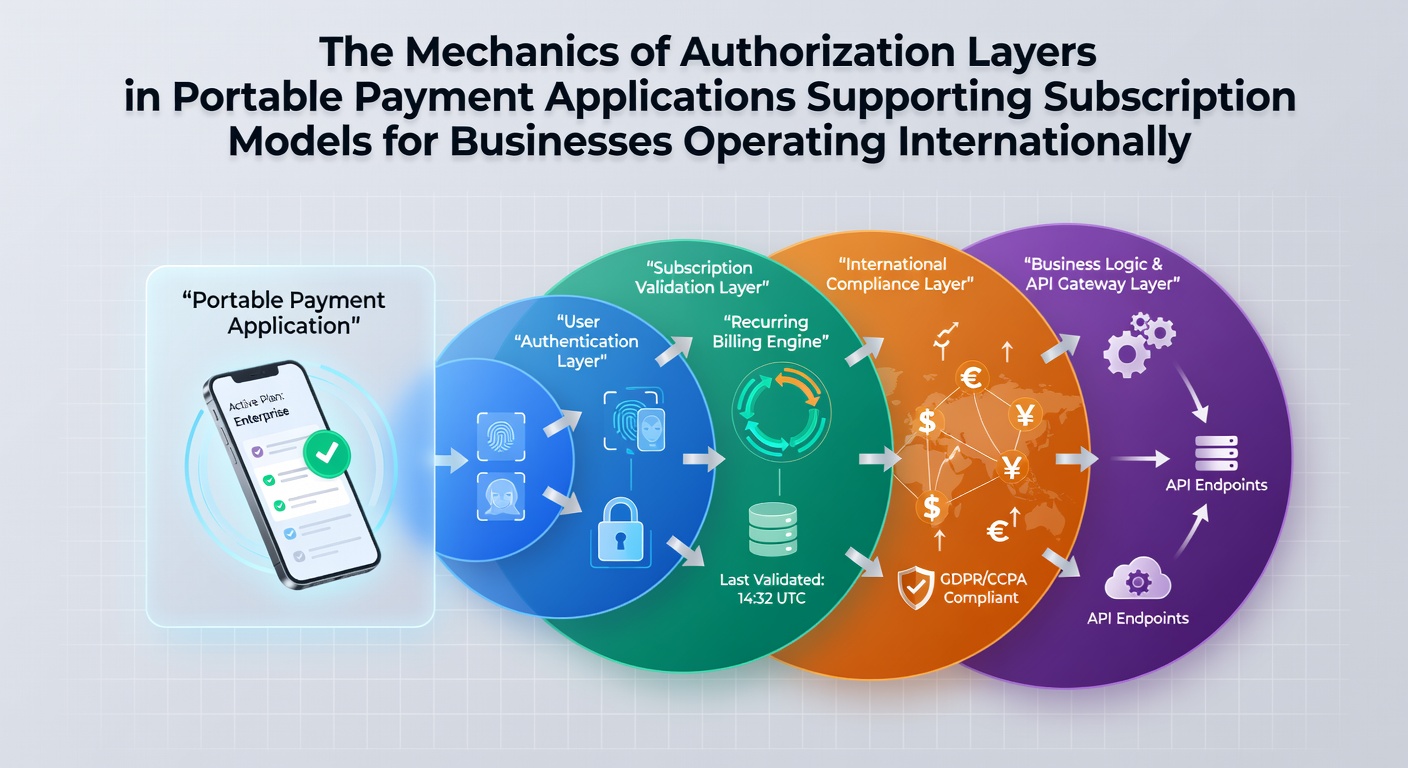

Portable payment applications manage authorization through multiple verification stages that confirm user identity, transaction validity, and compliance before funds move, and these processes become especially intricate when businesses handle recurring subscriptions across borders where regulations differ by region. Data from industry reports shows that such layers typically include initial device authentication, token generation for recurring charges, and ongoing risk scoring that adjusts based on location and transaction history.

Core Components of Authorization Layers

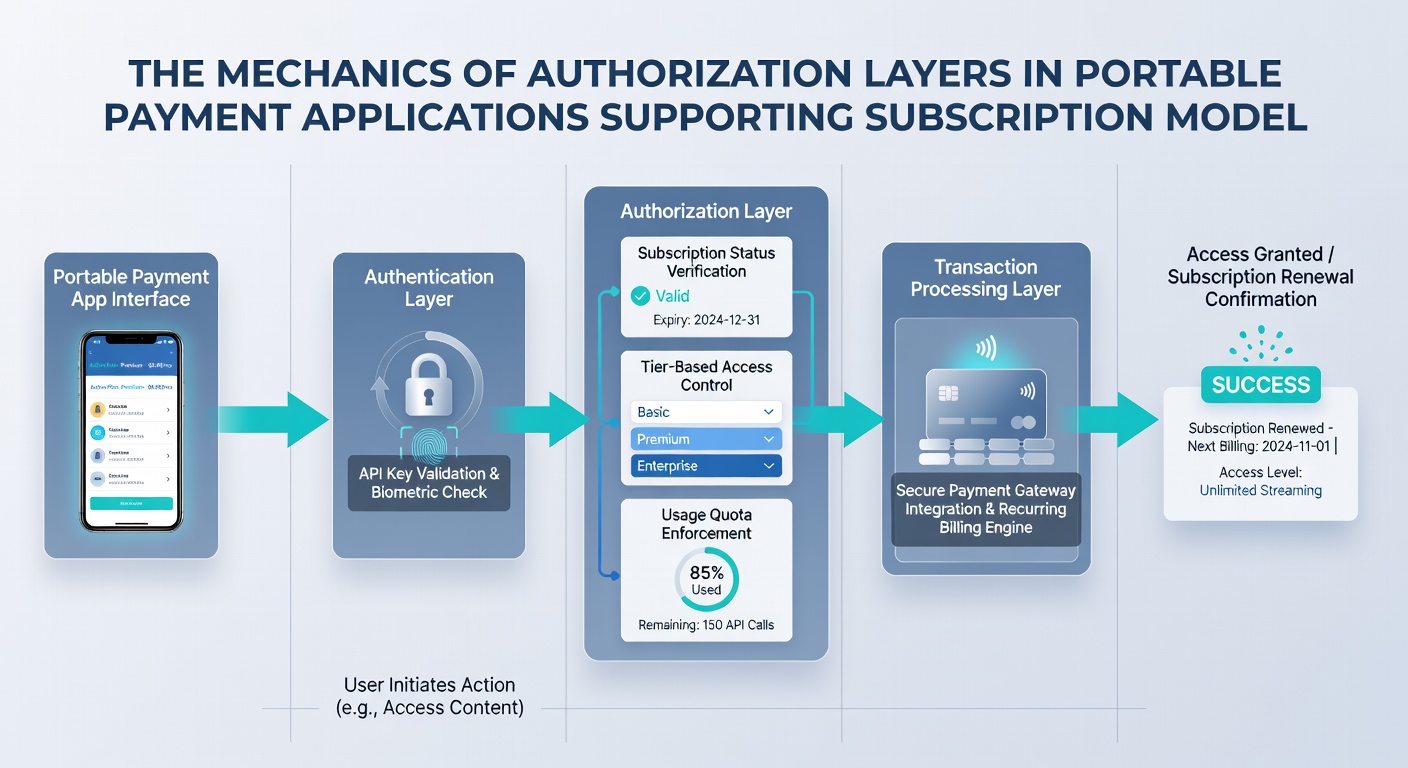

Authorization begins with user verification that combines device fingerprinting with biometric checks or PIN entry, after which the system generates a secure token that replaces sensitive card details for future billing cycles, and this tokenization approach reduces exposure while allowing seamless renewals. Observers note that portable apps often integrate with backend gateways that perform real-time checks against blacklists and velocity rules before approving each recurring charge.

Next comes the risk assessment phase where algorithms evaluate factors like IP address changes, spending patterns, and merchant category codes, and these evaluations run continuously to flag anomalies that might indicate fraud or account takeover attempts. Research indicates that subscription models benefit from pre-authorization holds that reserve funds without immediate capture, which helps businesses manage cash flow while complying with card network rules on recurring transactions.

Handling Recurring Subscriptions in Mobile Environments

Subscription support requires apps to store tokenized credentials that renew automatically according to fixed schedules, and the authorization layer validates each cycle against updated compliance requirements such as strong customer authentication mandates in various jurisdictions. Those who've studied payment flows observe that portable applications frequently employ scheduled job processors that trigger authorization requests hours before billing dates to allow time for retries if initial attempts fail due to network issues or temporary holds.

Token lifecycle management plays a central role since tokens expire or require refresh after certain periods or events like card replacement, and systems must re-authenticate users through the app interface when updates occur. Data shows that businesses operating internationally coordinate these refreshes with local payment schemes to avoid service interruptions during high-volume renewal periods.

International Operations and Regulatory Alignment

Cross-border operations introduce additional authorization steps that account for currency conversion, local tax reporting, and jurisdiction-specific security protocols, and applications must route requests through processors equipped to handle multiple settlement networks simultaneously. According to the Bank for International Settlements, payment systems in different regions maintain distinct authorization endpoints that require apps to adapt request formats dynamically based on the user's registered location and payment method origin.

By June 2026, updated standards from several central banks are expected to emphasize enhanced data sharing between issuers and acquirers for recurring transactions, which will likely influence how portable apps structure their verification sequences. Experts have observed that businesses already prepare for these shifts by implementing modular authorization engines that can incorporate new compliance checks without full system overhauls.

Multi-currency handling adds complexity because authorization amounts must convert accurately at the time of each charge while maintaining consistency with original subscription agreements, and apps use real-time exchange rate services to lock in values during the approval window. Those monitoring these systems report that failure to align conversions properly can trigger declines even when sufficient funds exist in the customer's account.

Security Protocols and Error Management

Encryption standards protect data in transit and at rest throughout the authorization chain, and portable apps commonly employ end-to-end encryption paired with certificate pinning to prevent interception on mobile networks. When declines occur the system logs specific response codes that guide retry logic or prompt users for updated details, which maintains service continuity for legitimate subscriptions.

Monitoring dashboards track authorization success rates across regions and flag patterns that might require adjustments to risk thresholds, and this data-driven approach allows businesses to refine their processes based on actual transaction outcomes rather than static rules. Research from the Financial Consumer Agency of Canada highlights how regional variations in decline reasons affect subscription retention when not addressed promptly through targeted authorization tweaks.

Conclusion

Authorization layers in portable payment applications form an interconnected system that balances security, compliance, and user convenience for international subscription businesses, and ongoing developments in standards will continue to shape how these mechanisms operate in practice. Companies that align their app architectures with evolving requirements position themselves to handle recurring charges reliably across diverse markets.